Passive Investing Bubble

One of the most used tools of the 21st century American Investor is the broad based Index Fund. Developed in the 1970’s by John Bogle, the founder of Vanguard, investing regularly in index funds has become one of the most popular investment strategies in the United States. Index funds now control roughly 50% of U.S. equity fund assets as compared to only 21% in 2012. Developed as a rebuttal against high active management fees and poor returns versus the larger S&P 500 market index, Vanguard created a fund that would offer diversification and lower fees, while providing consistent returns over the long term. Vanguard’s investment thesis was simple; create a fund composed of the same stocks and weightings of the S&P 500. Over time, Vanguard funds became so successful that other companies followed suit offering similar products and then eventually new products, such as ETFs that track specific sectors of the market.

However, as passive investing grows, some in the investment community are starting to raise alarms about the strategy.

The Efficient Market Hypothesis

To understand passive investing, we must understand the efficient market hypothesis upon which passive investing has been built. The general idea of the efficient market hypothesis is that stocks are fairly priced at all times and an investor is not able to find stocks that are “undervalued” or “overvalued” unless the investor is using information about the stock that is not public. This thesis assumes that all investors in the market have the same access to information and are incorporating all information to determine the stock price. This means that the only changes to stock prices are a result of new future information. Since no one is able to consistently predict the future, new information is considered random. This randomness of future information implies that in the long term, stock pickers are not able to consistently beat the market and investors are better off buying the entire market in the long run.

The Efficient Market Hypothesis has largely taken over modern financial theory with many today saying it is impossible to beat the market and everyone is better off investing in a low cost index fund.

Passive Investing

Passive investing is the idea that investors will invest money in the stock market at consistent intervals (every week, month, etc) and let the money compound over time. This strategy often uses a fund such as the Vanguard 500 index fund which buys the stocks that comprise the S&P 500 index according to the stock’s weighting in the index. A simple example of weighting is as follows; a company with a $1 Trillion Market Cap will receive more allocation than a company that has a $1 Billion Market Cap. Essentially the S&P 500 index has an aggregate value of all the stocks in the index and stocks that comprise a higher percentage of that total value will receive a higher weighting in the index and therefore a higher capital allocation in the index funds that track the index.

401ks are also an extremely popular passive investing vehicle. Almost 70 million Americans contribute to a 401k and in total $7.3 Trillion of assets are held in these investment vehicles. These investment vehicles automatically direct funds from American paychecks each month and park the money in a fund such as the U.S. Large Cap Equity fund which invests in the stocks of large U.S. Corporations. This means that millions of Americans already passively invest whether they are aware of the mechanism behind it or not.

Over the last 50 years, passive investing has taken over other popular saving strategies such as pensions, with only 7% of private employees having access to a pension. This shift has also partially been driven by legislation. Not only has legislation created the 401K with the Revenue Act of 1978, it has also expanded and supported the program with legislation such as “catch up” contributions in 2001 or legislation automatically enrolling employees in the program.

Americans have fully embraced the market and passive investing as the path to a comfortable future retirement.

Basic Market Mechanisms

To understand the risks with passive investing, the basic market mechanisms must first be understood.

A market is a place where buyers and sellers are able to exchange items and where prices are set by supply and demand. When there is more demand for a company, the price of the company stock rises as there are more buyers in the market than sellers. Traditionally, stock pickers will evaluate a company based on their financial statements and future prospects to determine the price of a stock. When the stock price is below the intrinsic value of the company, a stock picker will buy shares, and when the stock is trading for a price that is not supported by company fundamentals, they will sell.

Another important aspect of markets is that efficient markets need a balance of both buyers AND sellers. An imbalance of either can cause prices to be above or below their true value. This is an important note to keep in mind when talking about the issues with passive investing.

Current State of Passive Investing

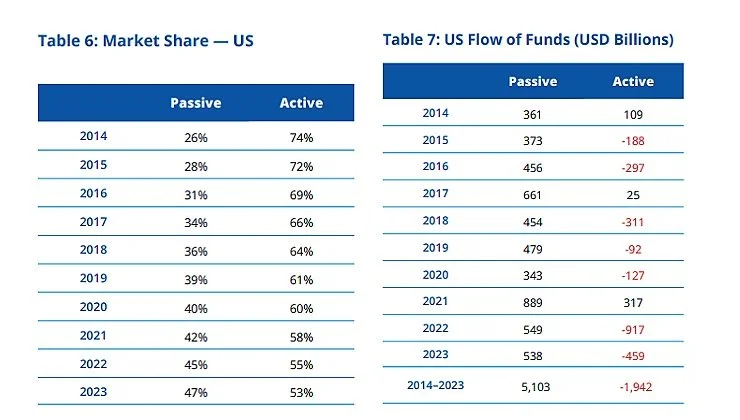

Table 6 shows the current market share of U.S Equity Fund Assets. As shown, passive investing has steadily risen from 26% of the market to 47% of the market in just 9 years. In the same time interval, active investing has lost market share of roughly that same amount and is barely hanging on to a majority. This growth in market share is further supported by Table 7 which shows hundreds of billions in fund inflows for passive while active has seen consistent outflows. These tables do not even include the $721 billion of fund inflows to passive in 2024.

Individuals who are passive investing are net buyers of assets on a consistent basis and are buyers who have a 40 to 50 year time horizon (meaning under most circumstances they do not sell for decades). This means that passive investors are buying roughly the same amount of stocks regardless if stocks are at all time highs or if the underlying company the stock represents is struggling. This can be an issue when a buyer goes to sell and realizes that the price they paid for the asset is nowhere near the price it is worth.

In efficient markets, buyers that drive up stock prices past a stock's underlying value are countered by sellers who see the stock is past its intrinsic value. A balance of buyers and sellers helps to keep assets around their fair market value. However, when the active sellers of the market (active managers) are replaced by passive investors, there is no one to counter the buying pressure of passive investors and the stock price goes past its intrinsic value. The only way to have the stock price to remain at its fair value in this situation is for the company to increase supply by issuing stock. Since many companies have compensation plans tied to the stock price, management is disincentivized to do so.

Passive investing may also be to blame for the historic concentration and overvaluation of the S&P 500’s top 7 holdings. The top 7 stocks of the S&P 500 account for roughly 33% of the total market cap of the index. Apple for example accounts for roughly 7% of the index. Apple has also been one of the most valuable companies since 2011. Assuming Apple received 7% of the $5.1 trillion of inflows, the company would have received roughly $350 billion or 10% of its current market cap. These inflows are going to a company that is currently trading at a premium P/E ratio 38 and a company that has single digit earnings growth below the S&P 500 average. Passive funds that are weighted similar to the S&P 500 distribute inflows disproportionately to the companies with the largest market caps regardless of fundamentals. Also, passive investors do not regularly sell which contributes to sock prices that may stay stuck at certain levels.

The biggest fear with passive investing is when passive investing flows start to turn negative with more outflows than inflows. If the current trends continue, the indiscriminate buying of passive investing will push asset prices to a level that no rational buyer will ever pay. This price level is further exacerbated if the transition from active to passive continues and active sellers have very little market share. This means that when net outflows start to occur, the price of the assets plummet as the potential buyers will never pay the price that is reflected in the market.

This is not to say that everyone who invests in passive funds should liquidate immediately or stop investing in their 401K. No one knows when net flows may turn negative and they may never turn negative. There is speculation that this will occur when the Baby Boomers start to liquidate, however that thesis has not come true with many believing that higher interest has allowed the retirees to live off interest. It remains to be seen when flows become negative, and until then, prices will keep appreciating as more sellers are driven out of the market and money keeps flowing into assets. In the meantime there are certainly opportunities. The Efficient Market Hypothesis does not take into account the basic behavioral finance of fear and greed. In times of Euphoria and Despair, stock prices often overshoot to the upside and downside respectively which leads to opportunities.

Remember: Past Performance is No Guarantee of Future Returns!

Disclaimer:

Be advised that investments may go up as well as down for any reason, and past performance of a stock is no guarantee of future performance.

Scarton Holdings makes no representation as to the timeliness, accuracy or suitability of any content on this website, and cannot be held liable for any irregularity or inaccuracy.

Stock recommendations and comments on this website are solely those of analysts and experts quoted. They do not represent the opinions of Scarton Holdings on whether to buy, sell or hold shares of any particular stock.

All investors are advised to conduct their own independent research before making an investment decision. Investors should consider the source and suitability of any investment advice for their needs. Your use of this website, and its content, is at your own risk.

Links from this website to third-party websites are in no way an endorsement by Scarton Holdings of their contents or their suitability for any purpose.